Personal finance is crucial for everyone. It impacts daily life and future security.

Understanding personal finance helps in managing money wisely. Good financial habits lead to stability and peace of mind. You can make informed decisions about spending, saving, and investing. This knowledge is key to achieving financial goals and avoiding debt. In this blog, we will explore the importance of personal finance.

We will see how it affects your life and why it’s essential for a secure future. By learning these basics, you can take control of your finances and build a better tomorrow. Let’s dive into the reasons why personal finance is so important.

Introduction To Personal Finance

Have you ever wondered why some people seem to have their finances all figured out while others struggle constantly? The answer often lies in personal finance. Understanding how to manage your money is crucial for a stable and happy life. Let’s dive into the basics of personal finance and see why it’s so important.

What Is Personal Finance?

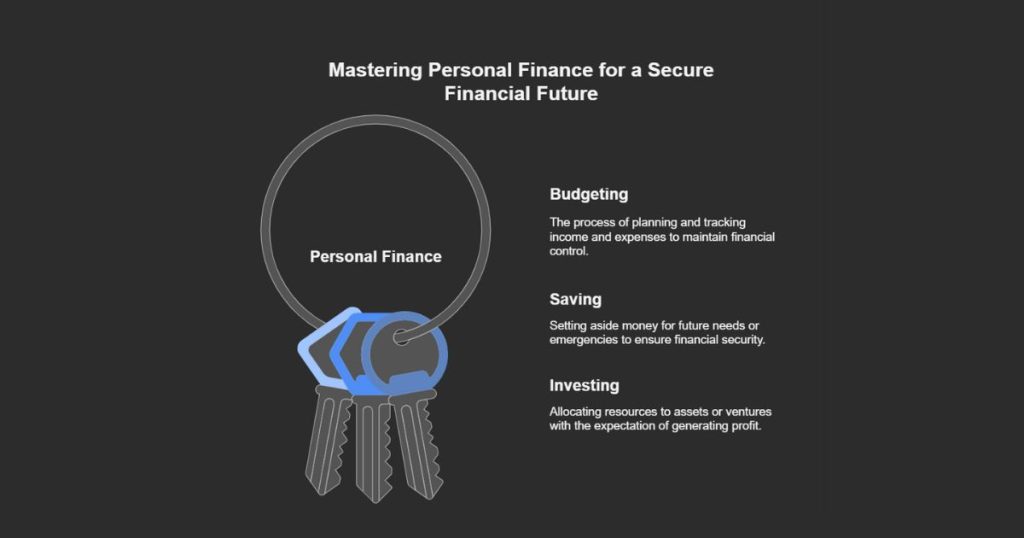

Personal finance is all about managing your money. It covers everything from budgeting and saving to investing and retirement planning. Think of it as the financial roadmap for your life. Without a good plan, it’s easy to get lost.

- Budgeting: Knowing where your money goes each month.

- Saving: Setting aside money for future needs.

- Investing: Making your money grow over time.

- Retirement planning: Ensuring you have enough money to live on when you stop working.

In a nutshell, personal finance is the skill of managing your money wisely, so you can achieve your financial goals.

Importance Of Financial Literacy

Financial literacy is the knowledge and skills needed to make smart money choices. Why is it so important? Let’s break it down:

- Better decision making: When you understand finances, you can make informed choices. For example, should you buy or rent a home?

- Avoiding debt: Knowing how to budget can help you avoid unnecessary debt. Credit card debt can be a real trap!

- Preparing for emergencies: Life is full of surprises, some good, some not so much. Having an emergency fund can keep you afloat during tough times.

Let’s face it, no one likes to worry about money. By becoming financially literate, you can reduce stress and enjoy a more secure and fulfilling life.

So, start learning about personal finance today. Your future self will thank you!

Budgeting Basics

Managing your personal finances can feel like navigating a maze, but understanding the basics of budgeting can make it simpler. Budgeting helps you take control of your money, ensuring you have enough for essentials while saving for the future. In this section, we will break down the basics of budgeting into easy-to-follow steps.

Creating A Budget

Creating a budget is the first step to managing your finances. Think of it as a roadmap for your money. Here’s a simple way to get started:

- List Your Income: Write down all sources of income. This includes your salary, any freelance work, or side gigs.

- Track Your Expenses: Note down everything you spend money on. This includes rent, groceries, utilities, and entertainment.

- Categorize Expenses: Group your expenses into categories like housing, food, transportation, and savings.

- Compare Income and Expenses: Subtract your total expenses from your total income. This will show you if you are living within your means or overspending.

Creating a budget may seem daunting at first, but it’s a crucial step towards financial freedom. It helps you see where your money is going and where you can make adjustments.

Tracking Expenses

Once you have a budget in place, the next step is to track your expenses. This ensures you stick to your budget and avoid unnecessary spending. Here are some tips:

- Keep Receipts: Hold onto receipts for all purchases. This helps you record expenses accurately.

- Use Apps: Consider using budgeting apps like Mint or YNAB (You Need A Budget). These apps help you track expenses in real-time and categorize them automatically.

- Set Reminders: Set reminders to update your budget regularly. This could be a weekly or monthly activity.

Tracking expenses might feel like a chore, but it’s a game-changer. It helps you stay accountable and make informed financial decisions. For instance, if you notice you’re spending too much on dining out, you can adjust by cooking more meals at home.

Remember, budgeting is not about restricting yourself but about making your money work for you. With a clear budget and a habit of tracking expenses, you will find it easier to achieve your financial goals. So, why wait? Start budgeting today and take the first step towards financial freedom.

Saving Strategies

Saving strategies are essential for managing personal finances effectively. They help individuals prepare for unexpected expenses and achieve their financial goals. By implementing smart saving techniques, you can ensure financial stability and peace of mind.

Emergency Fund

An emergency fund is crucial for handling unexpected expenses. Life is unpredictable. You might face sudden medical bills, car repairs, or job loss. Having an emergency fund ensures you can cover these costs without going into debt. Aim to save at least three to six months’ worth of living expenses. Keep this money in an easily accessible account.

Short-term And Long-term Goals

Setting short-term and long-term savings goals is important. Short-term goals might include saving for a vacation or a new gadget. Long-term goals could involve buying a house or retirement planning. Identify your goals and create a plan to achieve them. Break down your goals into manageable steps. Allocate a specific amount of your income toward each goal.

By focusing on these saving strategies, you can build a solid financial foundation. An emergency fund and clear goals will help you stay prepared and motivated. Start saving today and secure your financial future.

Investing Essentials

Understanding personal finance is crucial for everyone, but investing is one of its most important aspects. Investing can grow your wealth over time and provide financial security. But where should you start? Let’s dive into some of the essentials of investing.

Types Of Investments

There are many ways to invest your money, and knowing the different types can help you make informed decisions:

- Stocks: Owning shares in companies. Stocks can offer high returns but come with higher risks.

- Bonds: Loans to companies or governments. Bonds are generally safer than stocks but offer lower returns.

- Mutual Funds: Pools of money from many investors. Managed by professionals, these funds invest in a mix of stocks, bonds, or other assets.

- Real Estate: Buying property to rent out or sell later. This can provide steady income and potential appreciation.

- ETFs (Exchange-Traded Funds): Similar to mutual funds but traded on stock exchanges. ETFs can be a good way to diversify your portfolio.

Risk Management

Investing always comes with risks. But don’t worry; there are ways to manage those risks:

- Diversification: Don’t put all your eggs in one basket. Spread your investments across different assets to reduce risk.

- Research: Understand what you’re investing in. Read up on the companies or funds, and don’t be afraid to ask questions.

- Time Horizon: Think about how long you can leave your money invested. Longer time horizons often allow for more risk since you have time to recover from any downturns.

- Emergency Fund: Always keep some money in a safe, easily accessible place. This can help you avoid selling investments at a bad time.

Investing can seem daunting at first, but remember, everyone starts somewhere. With some basic knowledge and careful planning, you can make your money work for you. So, why not start today?

Debt Management

When it comes to personal finance, one of the most crucial aspects is debt management. Understanding how to manage debt effectively can be the difference between financial stress and financial freedom. Let’s dive into the essentials of debt management, focusing on how to discern good debt from bad debt and how to create effective debt repayment plans.

Good Vs. Bad Debt

Not all debt is created equal. There is such a thing as good debt and bad debt. Sounds interesting, right?

Good debt is generally considered an investment that will grow in value or generate long-term income. For example, taking out a mortgage to buy a home or a student loan to pay for education. These types of debt can be seen as stepping stones to a better future.

On the flip side, bad debt refers to money borrowed to purchase depreciating assets or for consumption rather than investment. Credit card debt, high-interest loans, and auto loans often fall into this category. These can quickly spiral out of control if not managed properly.

Debt Repayment Plans

So, you’ve identified your debts. Now what? It’s time to tackle them head-on with a solid debt repayment plan. Here are a few strategies to consider:

- Debt Snowball Method: Focus on paying off the smallest debts first while making minimum payments on larger ones. This can give you quick wins and build momentum.

- Debt Avalanche Method: Pay off debts with the highest interest rates first, which can save you more money in the long run.

- Debt Consolidation: Combine multiple debts into a single loan with a lower interest rate. This can simplify your payments and reduce overall interest costs.

Creating a debt repayment plan doesn’t just help you pay off debt; it also gives you a sense of control and direction. It’s like having a roadmap for your financial journey. And remember, sticking to your plan requires discipline and sometimes sacrifices, but the end goal is financial freedom.

In conclusion, managing debt effectively is a cornerstone of personal finance. By understanding the difference between good and bad debt and implementing a robust repayment plan, you’re well on your way to achieving financial stability and peace of mind.

Retirement Planning

Planning for retirement is crucial for a secure future. It ensures you have enough money to live comfortably when you stop working. Without a good plan, you might face financial stress during your golden years.

Retirement Accounts

Retirement accounts are essential tools for saving money. These accounts offer tax benefits and help your savings grow over time. Popular options include 401(k), IRA, and Roth IRA. Each has unique features and benefits.

A 401(k) is often provided by employers. It allows you to save money from your paycheck before taxes. An IRA is an individual account that offers tax advantages. You can open it at most financial institutions. A Roth IRA is similar but offers tax-free withdrawals in retirement.

Saving For The Future

Saving for the future is important for a comfortable retirement. Start saving early to take advantage of compound interest. Small, regular contributions can grow significantly over time.

Set a savings goal based on your retirement needs. Consider factors like living expenses, healthcare costs, and travel plans. Use a retirement calculator to estimate how much you need to save. Stick to a budget to ensure you save consistently.

Insurance And Protection

When it comes to managing your money, one aspect that often gets overlooked is insurance. But, have you ever wondered why insurance and protection are so important? Let’s break it down. Insurance acts as a safety net, protecting you and your loved ones from financial hardships. It’s like having an invisible shield that can absorb the shock of unexpected events, such as accidents, illnesses, or natural disasters. Let’s dive deeper into this topic to understand why insurance should be a vital part of your personal finance strategy.

Types Of Insurance

There are various types of insurance, each serving a unique purpose. Here are a few common ones:

- Health Insurance: This covers medical expenses. If you fall sick or need surgery, it helps pay for those costs.

- Life Insurance: This provides financial support to your family if you pass away. It can help cover funeral costs and provide a financial cushion.

- Car Insurance: If you own a car, this is a must. It covers damages from accidents, theft, or natural disasters.

- Home Insurance: This protects your home and its contents against risks like fire, theft, and natural calamities.

- Travel Insurance: When you’re traveling, this covers unexpected events like trip cancellations, lost luggage, or medical emergencies.

Importance Of Coverage

Now, you might be wondering, “Do I really need all this coverage?” The answer is a resounding yes! Here’s why:

- Financial Security: Insurance provides a financial safety net, helping you manage risks and uncertainties without draining your savings.

- Peace of Mind: Knowing you are covered allows you to live your life more freely, without constantly worrying about what could go wrong.

- Legal Requirements: Some types of insurance, like car insurance, are mandatory by law. Not having it can result in hefty fines and legal issues.

- Protection of Assets: Your home, car, and other valuable assets are protected, ensuring that you don’t face devastating losses.

Imagine if you had to pay for a major surgery out of pocket. Or if your house was damaged in a storm and you had no way to repair it. Insurance helps you avoid these stressful situations. It’s like having a superhero in your back pocket, ready to jump in and save the day when things go sideways.

In conclusion, incorporating insurance into your personal finance plan is not just smart; it’s essential. It provides peace of mind, financial security, and protection for you and your loved ones. Don’t wait for a disaster to strike. Get covered and stay protected!

Building Wealth

Building wealth is a crucial aspect of personal finance. It involves creating assets that grow over time. The goal is to increase financial security and achieve financial freedom. But how does one go about building wealth? Two key strategies stand out: generating passive income and exploring entrepreneurial ventures.

Passive Income

Passive income is money earned with minimal effort. It often comes from investments. Examples include dividends from stocks, rental income from properties, or interest from savings accounts. Passive income allows you to earn money while you sleep. It can supplement your regular income. This extra income helps in paying off debts, saving for retirement, or investing further.

Entrepreneurial Ventures

Starting your own business can be a path to building wealth. Many successful entrepreneurs started with small ventures. With determination and smart planning, they grew their businesses. Owning a business allows you to control your financial destiny. You can reinvest profits to expand. This can lead to significant wealth over time. Whether it’s a side hustle or a full-time job, entrepreneurship offers vast opportunities.

Financial Independence

Financial independence is a crucial aspect of personal finance. It allows you to live life on your own terms. By managing your money wisely, you gain control over your financial future. This leads to a stress-free and fulfilling life.

Achieving Financial Freedom

Achieving financial freedom means having enough savings and investments to support your lifestyle. This eliminates the need to rely on a paycheck. It allows you to pursue your passions without financial worries. You can spend more time with family and friends.

Building a strong financial foundation starts with budgeting. Knowing where your money goes helps you cut unnecessary expenses. Saving and investing are also key steps. They help your money grow over time.

Living A Debt-free Life

Living a debt-free life provides immense relief. Debt can be a heavy burden, causing stress and limiting your choices. Paying off debts should be a priority. It frees up more of your income for saving and investing.

Debt-free living also improves your credit score. A good credit score opens doors to better financial opportunities. You can secure loans with lower interest rates. This saves you money in the long run.

Embrace a debt-free lifestyle. It brings peace of mind and financial security. You can focus on building wealth and enjoying life.

Frequently Asked Questions

Why Do You Think Personal Finance Is Important?

Personal finance is crucial for managing money effectively, achieving financial goals, and ensuring long-term financial security. It helps reduce debt, increase savings, and plan for retirement. Proper financial management improves overall quality of life.

Why Is Personal Finance An Essential Life Skill?

Personal finance is essential because it helps you manage money effectively. It ensures financial stability, reduces stress, and prepares for emergencies. Understanding personal finance enables better saving, investing, and budgeting. This skill promotes informed financial decisions, leading to a secure and prosperous future.

Why Is It Important To Plan Personal Finance?

Planning personal finance helps manage money effectively, reduces financial stress, and ensures long-term financial stability. It enables better budgeting, saving, and investing.

What Is Finance And Why Is It Important?

Finance is the management of money, investments, and financial planning. It’s crucial for making informed decisions, ensuring stability, and achieving growth.

Conclusion

Personal finance is crucial for a stable life. It helps you manage money wisely. You can plan for future needs and avoid debt. Saving money provides security and peace of mind. Investing smartly can grow your wealth over time. Understanding personal finance boosts confidence and reduces stress.

Make informed decisions and achieve financial goals. Start small, but stay consistent. Your future self will thank you.