Personal finances involve managing your money wisely. This includes budgeting, saving, investing, and planning for the future.

Understanding personal finances is crucial. It helps you make informed decisions about your money. Good financial habits can lead to a secure and comfortable life. Poor financial management, however, can cause stress and hardship. Knowing the basics can be empowering.

It allows you to take control of your financial future. Whether you are just starting out or looking to improve your financial situation, learning about personal finances is key. This blog will explore the essentials, providing you with valuable insights to manage your money better. From setting financial goals to understanding credit, we will cover it all. Get ready to take charge of your finances!

Introduction To Personal Finances

Managing your money is one of the most important skills you’ll ever learn. Personal finances involve everything from budgeting and saving to investing and planning for retirement. It’s a broad term that encompasses all the financial decisions you make throughout your life. Understanding personal finances is the first step to financial freedom and security.

Importance Of Financial Literacy

Do you know how to make your money work for you? Financial literacy is about understanding how money works, and how you can make it grow. Without this knowledge, it’s easy to fall into debt or make poor investment choices.

Consider this: if you don’t understand interest rates, you might end up paying much more than you borrowed. Or if you don’t know how to budget, you could find yourself living paycheck to paycheck. Financial literacy empowers you to make informed decisions and avoid costly mistakes.

Benefits Of Money Management

Effective money management can transform your life. When you control your finances, you reduce stress and increase your peace of mind. You’ll know exactly where your money is going and how much you need to save for your goals.

Imagine being able to handle an unexpected expense without panic. That’s the power of having an emergency fund. Or think about retiring comfortably because you started saving early. Good money management isn’t about being rich; it’s about being prepared and making your money work for you.

Ask yourself: How can I improve my financial literacy today? What steps can I take to manage my money better? Start small, and gradually build your knowledge and skills. Your future self will thank you.

Setting Financial Goals

Setting financial goals is a crucial part of managing personal finances. These goals help you plan your future and ensure financial stability. They act as a roadmap, guiding your spending and saving habits. By setting clear financial goals, you can track your progress and stay motivated. Let’s explore the types of financial goals you can set.

Short-term Goals

Short-term goals are those you aim to achieve within a year. They are usually smaller, more immediate financial targets. Examples include saving for a vacation, paying off credit card debt, or building an emergency fund. Setting short-term goals helps you make quick progress and gain confidence in managing your money.

Long-term Goals

Long-term goals take more time to accomplish. They are usually set for periods longer than a year. Examples include saving for retirement, buying a house, or paying off student loans. Long-term goals require consistent effort and planning. They often involve larger sums of money and more complex strategies.

Creating A Budget

Creating a budget helps manage personal finances effectively. It tracks income, expenses, and savings goals. This practice ensures financial stability and better money management.

Creating a budget is a crucial step in managing your personal finances effectively. It allows you to gain control over your money, ensuring that you have enough to cover your expenses while saving for future goals.

Tracking Expenses

Tracking your expenses is the first step in creating a budget. Start by keeping a record of everything you spend money on for a month. Use a notebook, an app, or a spreadsheet. You might be surprised to see where your money is going.

Categorize your expenses into different areas like food, transportation, entertainment, and bills. This helps you see which areas you might need to cut back on.

Allocating Funds

Once you’ve tracked your expenses, it’s time to allocate funds. Determine how much money you have coming in each month and compare it to your expenses.

Create categories for essential expenses such as rent, utilities, groceries, and transportation. Allocate funds to these categories first.

Then, set aside money for savings and investments. Finally, allocate funds for non-essential expenses like dining out and entertainment.

Creating a budget is not just about restricting yourself but about prioritizing your financial goals. Are you saving for a vacation or trying to pay off debt? Your budget should reflect these priorities.

Remember, a budget is a living document. Review it regularly and make adjustments as needed. By tracking your expenses and allocating funds wisely, you can take control of your finances and work towards your financial goals.

Saving Strategies

Personal finances involve managing your money through budgeting, saving, and investing. Effective saving strategies help build financial security and achieve long-term goals. Make a plan to spend wisely and save regularly.

When it comes to managing personal finances, saving strategies are essential. These strategies help you build a financial cushion and prepare for the future. By effectively managing your savings, you can achieve your financial goals faster and reduce stress.

An emergency fund is your financial safety net. It’s money set aside to cover unexpected expenses like medical bills, car repairs, or job loss. Ideally, you should aim to save three to six months’ worth of living expenses.

You might wonder, “How can I start?” Begin by setting small, achievable goals. For instance, aim to save $500 initially. Once you reach this milestone, gradually increase the amount.

Consistency is key. Set up automatic transfers from your checking to your emergency fund each month. This way, you save without even thinking about it.

Choosing the right savings account is crucial for your financial health. Not all savings accounts are created equal. Look for accounts with high-interest rates to maximize your earnings.

Consider online banks. They often offer better interest rates than traditional banks because they have lower overhead costs.

Think about your savings goals. Are you saving for a vacation, a new gadget, or perhaps a home down payment? Different goals might require different types of savings accounts. For short-term goals, a regular savings account might suffice. For long-term goals, explore options like Certificates of Deposit (CDs) or high-yield savings accounts.

To stay motivated, track your progress. Many banks offer tools to help you visualize your savings growth. Seeing your funds increase can be incredibly rewarding.

Have you ever wondered how much more you could save with just a slight change in habits? Small adjustments, like cutting down on dining out or canceling unused subscriptions, can significantly boost your savings.

Remember, saving is a journey, not a sprint. Celebrate your progress, no matter how small, and keep pushing towards your financial goals.

Investing Basics

Personal finances involve managing your money, including budgeting, saving, and investing. Understanding these basics helps you make informed decisions and plan for the future.

Investing can seem overwhelming at first, but understanding the basics can make it much easier. It’s about putting your money to work to grow over time. Let’s break it down step by step.

There are several types of investments you should be aware of. Stocks represent ownership in a company and can grow in value over time. Bonds are like loans you give to companies or governments, and they pay you interest.

Real estate involves buying property to rent or sell. Mutual funds pool money from many investors to invest in a diversified portfolio.

Each type has its own benefits and risks.

Managing risk is crucial to successful investing. Diversification is one way to manage risk. It involves spreading your investments across different types of assets.

Consider your risk tolerance. How much risk are you comfortable with? Younger investors might take more risks, aiming for higher returns over time.

Regularly review your investments. Adjust them as needed to keep your risk in line with your goals.

Investing can be a powerful tool for building wealth. Start small, learn as you go, and stay consistent. What investment types interest you the most?

Managing Debt

Managing debt is a key part of personal finances. It involves budgeting, paying bills on time, and reducing high-interest loans.

Managing debt is a crucial part of personal finances. Debt can easily spiral out of control if not properly managed. However, with the right strategies, you can take control of your debt and even use it to your advantage.

Types Of Debt

Not all debt is created equal. Understanding the types of debt you have is the first step in managing it effectively.

There are two main types of debt: secured and unsecured. Secured debt is backed by an asset, like a house or car. If you fail to pay, the lender can take the asset. Examples include mortgages and auto loans.

Unsecured debt, on the other hand, is not tied to any specific asset. Credit card debt and student loans fall into this category. Because it’s riskier for lenders, it often comes with higher interest rates.

Debt Repayment Plans

Once you know what kind of debt you have, the next step is creating a repayment plan. This can help you pay off debt faster and save money on interest.

One effective method is the debt snowball approach. Start by paying off your smallest debt first while making minimum payments on larger debts. This can give you a quick win and motivate you to tackle the next one.

Another method is the debt avalanche. Focus on paying off the debt with the highest interest rate first. This can save you more money in the long run.

You might also consider consolidating your debts. This means taking out a new loan to pay off multiple debts. This can simplify your payments and sometimes lower your interest rates.

Managing debt can feel overwhelming, but it’s all about taking small, manageable steps. What’s one small step you can take today to get a handle on your debt?

Building Credit

Personal finances include building credit, which is essential for obtaining loans and favorable interest rates. Good credit opens doors to better financial opportunities. Managing credit responsibly impacts overall financial health.

Building credit is a crucial part of managing your personal finances. A good credit history can open doors to better interest rates on loans, credit cards, and even influence your ability to rent an apartment or get a job. Whether you are just starting or rebuilding, understanding and improving your credit is essential.

Understanding Credit Scores

Your credit score is a three-digit number that represents your creditworthiness. It’s based on your credit history, which includes your payment history, amounts owed, length of credit history, types of credit used, and new credit inquiries.

A higher score means you are seen as less risky by lenders. Scores generally range from 300 to 850.

A score above 700 is considered good, while anything above 800 is excellent.

Regularly check your credit report to ensure accuracy. Mistakes can drag your score down.

Improving Credit

Improving your credit takes time and consistency, but it’s totally achievable. Start by paying your bills on time. This is the most significant factor in your credit score.

Next, reduce your credit card balances. High balances can negatively impact your score. Aim to keep your utilization below 30%.

If you don’t have credit, consider getting a secured credit card. These cards require a deposit, which becomes your credit limit. Use it responsibly to build your credit history.

Avoid opening too many new accounts at once. Each application results in a hard inquiry, which can temporarily lower your score.

Have you thought about setting up automatic payments? This ensures you never miss a due date, which can boost your score over time.

Building credit is a step-by-step process. Each small action adds up to create a stronger financial future for you.

Protecting Your Finances

Protecting your finances is a crucial aspect of personal finance management. It involves taking steps to safeguard your money from unexpected events and fraud. This ensures that your hard-earned savings remain secure and available when you need them most. Let’s explore some key areas to focus on.

Insurance Options

Insurance is one of the best ways to protect your finances. There are various types of insurance policies available. Health insurance covers medical expenses. Life insurance provides financial support to your family in case of your death. Auto insurance helps with car accident costs. Home insurance protects your property from damage. Each type of insurance serves a unique purpose. Choose the right ones based on your needs and lifestyle.

Fraud Prevention

Fraud can have a significant impact on your finances. It’s important to take steps to prevent it. Monitor your bank statements regularly. Report any suspicious activity immediately. Use strong, unique passwords for online accounts. Be cautious when sharing personal information. Avoid clicking on unknown links or emails. By staying vigilant, you can protect yourself from financial fraud.

Using Financial Tools

Managing personal finances can seem overwhelming. Using financial tools can simplify the process. These tools help track expenses, budget, and invest wisely. They offer a clear view of your financial health.

Budgeting Apps

Budgeting apps are essential for managing money. They track income and expenses. Users can set financial goals and monitor progress. Many apps categorize spending, making it easy to see where money goes. Alerts and notifications help stay on track. Popular apps include Mint and YNAB. They are user-friendly and offer valuable insights.

Investment Platforms

Investment platforms provide access to various investment options. They help users grow their money. These platforms offer tools to research stocks, bonds, and mutual funds. Some platforms offer robo-advisors for automated investing. This is useful for beginners. Examples include Robinhood and ETRADE. These platforms are secure and easy to use.

Reviewing And Adjusting Financial Plans

Personal finances are essential for everyone, guiding how we manage money, save, and plan for the future. One critical aspect is reviewing and adjusting financial plans. This process ensures your financial health stays strong, adaptable, and aligned with your goals.

Regular Financial Check-ups

Think of your finances like your health. Regular check-ups are vital. Set a specific time, perhaps monthly or quarterly, to review your financial status.

Check your expenses, savings, and investments. Are you spending too much on non-essential items? Are your savings growing? Is your investment portfolio healthy?

Adjust your plans based on these insights. If you spent too much last month, cut back on unnecessary expenses. If your savings aren’t growing, consider increasing your contributions.

Adapting To Life Changes

Life is full of changes. Marriage, having children, new job, or retirement impact your finances significantly.

Each change requires adjustments to your financial plans. After getting married, you might need to combine finances and set joint goals. Having a child means budgeting for extra expenses like childcare and education.

Be proactive. Anticipate life changes and adjust your financial plans accordingly. This keeps you prepared and ensures a smooth transition during these changes.

Have you ever faced a financial setback? How did you adjust your plans? Share your experiences and help others learn from them!

Frequently Asked Questions

What Is Personal Finance?

Personal finance involves managing your money, including budgeting, saving, investing, and planning for retirement. It ensures financial security and growth.

What Do You Mean By Personal Finance?

Personal finance refers to managing individual financial activities, including budgeting, saving, investing, and planning for retirement. It involves decisions about income, expenses, and financial goals.

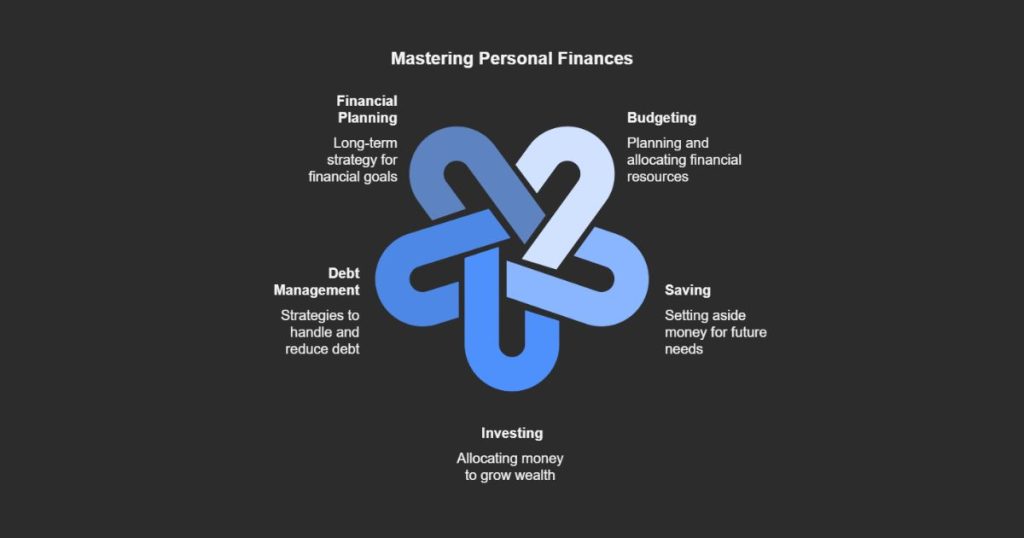

What Are The 5 Points Of Personal Finance?

The 5 points of personal finance are budgeting, saving, investing, debt management, and retirement planning. These elements help manage money efficiently.

What Is The 50/30/20 Rule In Finance?

The 50/30/20 rule in finance allocates 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. This budgeting method helps manage finances effectively.

Conclusion

Understanding personal finances is essential for everyone. It helps manage money wisely. Budgeting, saving, and investing are key components. Small changes lead to big results. Start with a plan. Stick to your goals. Learn more to improve your financial health.

Every step counts. Make informed decisions. Achieve financial stability and peace of mind. Your future self will thank you.